EX-99.1

Published on April 21, 2026

Exhibit 99.1

April 21, 2026

Fellow Shareholders,

For the first quarter, we recorded net income to common stockholders of $5.6 million, or $0.23 per diluted share. Transportation revenue growth was 0.6% in 1Q 2026 vs. 4Q 2025. Historically, we have experienced a high single digit decline between 4Q and 1Q due to seasonality. We view net revenue growth in this quarter's results as a positive signal that we have only experienced once before in the past decade.

CEO Summary: The Metrics That Matter Most

| North Star Metrics | Long-Term Target | Qtr Ending 3/31/26 | |||||||||

| Transportation Revenue Growth* | > 15% | 23.5 | % | ||||||||

| Factoring Operating Margin | > 40% | 34.7 | % | ||||||||

| Payments EBITDA Margin (ex-LoadPay) | > 50% | 34.0 | % | ||||||||

| Intelligence Gross Margin | > 85% | 86.1% | |||||||||

* Growth figures are YoY, all other metrics are as of the quarter end.

This is a new and simple table for investors. We added it because key performance indicators change as we build out the Payments Network and our transactional platform. We used to talk about logos, density, and product roadmap; we now talk about revenue growth and margin. This does not mean we have stopped innovating or pursuing growth — it means we expect those efforts to show up in our numbers. We will continue putting forth the KPIs that we believe are the best signal of achieving long-term value creation. Investors will be able to judge both the merit of our recommended KPIs and our performance against them.

Our North Star. If we achieve our revenue growth and margin targets expressed in the table above, and all other things remain equal (which rarely happens!), we should generate roughly $1.00 of incremental earnings annually. That is where the North Star leads us. The purpose of investing in our Network and platform over the last several years, including through a very long and difficult cycle, was so that we could deliver value to our customers that compounds earnings for our investors.

These metrics will be influenced by factors outside of our control — cyclicality, seasonality, regulation, interest rates, and geopolitics to name a few. We cannot and will not manage the business to short-term fluctuations, whether cyclical or seasonal, but we will report on our progress with a focus on sustained improvement and performance that builds durable value over time.

What are the performance drivers to achieve our North Star? While the targets above define the outcomes, how we manage the business beneath them is equally important. We will continue to report legacy metrics within the letter, but expect that we will emphasize the following.

Factoring – Our target for the year 2026 is to grow revenue in the low teens for this segment and to achieve our long-term >40% margin target exiting the year. In addition to these North Star metrics, we will also report on (i) customer growth, (ii) volume growth, and (iii) product attachment ratio ("PAR") for the reasons discussed below.

•Rationale for Margin Target: A 40% operating margin is rare air in commercial finance. To consistently achieve that margin usually requires proprietary data, embedded distribution, and network effects. As such, it deserves a different multiple than traditional finance because it performs more like a transactional platform than a lending business. With that platform comes high margin add-on business opportunities, including FaaS, Intelligence, and LoadPay.

◦To be clear, we report operating margin inclusive of funding costs. Not all operating margins in commercial finance are created or reported equally. If companies report operating income before cost of funds, it inflates apparent margins but obscures the true economics of the transaction. We measure

1

margin in our factoring segment after credit losses and operating expenses, and in a manner that reflects the full cost of delivering the service.

•Customer & Volume Growth: Which is more valuable for long-term value creation — customer growth or volume growth? This is not a simple answer. Both are valuable for different reasons. I can say with certainty that 500 owner/operator ("O/O") clients contribute more to our margin than a single customer with a fleet of 500 trucks. This discussion may sound familiar to pre-pandemic shareholders, as we moved away from reporting customer counts years ago as scale and mix dynamics made that measure less useful at predicting revenue in the segment. Times change, and our investments in technology have materially changed our cost of service and customer acquisition for O/Os and smaller fleets. We also offer products and services beyond working capital and smaller fleets are more likely to consume the entire bundle. If we can help smaller fleets thrive, our revenue scales with the economic value of each transaction more than just truck counts. As a result, we now think customer growth is a key indicator of long-term value creation that should be reported alongside of volume growth.

•PAR: Because multiple product attachment by our carriers is key to broadening the economic value of the carrier relationship, and because it often extends the duration of the carrier relationship, we are including PAR as a measure of our effectiveness at cross-selling. PAR examines our carrier customer universe against the three main Triumph factoring products: Factoring, LoadPay, and Fuel Cards, and will be expressed as a number out of a possible three.

Core Payments – Our target for the year is to grow revenue by 20% for this segment and, ex-LoadPay, achieve a ~40% EBITDA margin target exiting 2026. In addition to these North Star metrics, we will also report (i) PAR and (ii) revenue per invoice for the reasons discussed below.

•Rationale for Margin Target: A 50% EBITDA margin in our core Payments offering is a very strong midpoint for this business. While it does not reach the margin performance of the card networks, we believe it is positioned at the top end of other scaled payments platforms. When we add the current YoY revenue growth for core Payments (23.1%) plus the current EBITDA margin ex-LoadPay investments (34.0%), the sum approaches a “Rule of 60” business.[1] A business approaching the Rule of 60 reflects both growth and profitability, signaling a model capable of generating durable and compounding shareholder returns.

◦We break out LoadPay from our overall Payments segment so investors can see returns both inclusive and exclusive of the investments associated with LoadPay. Over the long run, we expect LoadPay, which is in its early stages, to be accretive to Payments margins.

•PAR: Our Payments products generate audit and payment fee revenue as well as quickpay and embedded working capital finance revenue. When customers adopt multiple products and use our banking payment rails, the margins are better, and it creates network effects that Payments or Audit alone do not. PAR examines our customer universe against the three main Triumph broker products: Payments, Audit, and Intelligence, and will be expressed as a number out of a possible three. When a broker adds Payments alongside Audit, or Intelligence services to either, we are not just adding new revenue — we are deepening the relationship and strengthening the network effects for every other participant. That is the compounding dynamic which segment economics alone do not reveal.

•Revenue per Invoice: Another important value driver is our ability to monetize the invoice in multiple ways for our broker customers, even across segments, as we add value through each touch. As such, the best way to track our progress is by the revenue generated per broker invoice, which we define as the revenue generated by our Payments, Audit, and Intelligence services to brokers divided by the number of unique invoices associated with those revenues. This metric captures our new business development, cross-sell success, and repricing efforts without getting lost in the details of a dozen other metrics to determine progress. Coupling this metric with our focus on growing both EBITDA margin and earnings contribution, ensures new revenue is created efficiently.

LoadPay - Our target for the year is to grow accounts by over 120% and revenue by 150% exiting 2026. In addition to these metrics, we will also report (i) revenue per account and (ii) revenue per active carrier account for the reasons discussed below.

2

•Rationale for 2026 Targets: LoadPay operates inside our Payments segment as an early-stage venture. To this point, we have focused on growth in customer accounts and the revenue per linked and funded account. We continue to believe this is the best measure of future value, but that these accounts are better described as "active carrier accounts." A LoadPay active carrier account is defined as one that is linked to Triumph Factoring or Payments and has been funded through the Triumph Network. Though LoadPay is only a little over one year old, those two metrics have been helpful in determining progress through the initial product rollout.

•Revenue per Account/Active Carrier Account: We believe these two metrics are effective in tracking our progress. These metrics require reporting total account growth as well as active carrier account growth allowing visibility into our success in converting carriers between these two cohorts. The revenue per active carrier account should be a better reflection of the long-term opportunity than revenue per account as customer behavior changes through using LoadPay as a primary operating account. To be frank, we are all still learning about the revenue opportunity inside of LoadPay as we roll out features and test things that have not yet been done by a financial institution at scale within the trucking industry. The uncertainty is what adds excitement to the opportunity — we are not afraid to do new things, and our new things are directed at very large markets. In sum, these metrics will communicate to investors how we are scaling the product, the value of attached services to the carrier, and how these unit economics are accretive to our Payments segment EBITDA margin target of > 50%.

Intelligence - Our target for the year is to grow revenue materially for this segment and maintain a > 85% gross margin target exiting 2026. In addition to this North Star metric, we will also report (i) annual recurring revenue ("ARR"), (ii) net revenue retention ("NRR"), and (iii) EBITDA margin for the reasons discussed below.

•Rationale for Gross Margin Target: A gross margin in our Intelligence segment that exceeds 85% positions it alongside the best data businesses for this metric. It is not normal for an early-stage data product to achieve this metric; however, because our Intelligence segment is connected to our Network, we have been able to do so. A gross margin at > 85% reflects high incremental margins, a low marginal cost to serve, and differentiated data.

•Revenue Growth: We have spent a year incorporating the technology we purchased from Greenscreens into our technology stack. This has been a time-consuming process. It is worth noting here the reinforcing value chain discussed in prior shareholder letters, where client growth in other segments enriches the Network data fueling Intelligence, creating a reinforcing loop which increases product value for the same customers. While Intelligence is a great product to help win and retain business, it must also stand on its own and generate material growth in revenue off of its current base.

•ARR, NRR, and EBITDA Margin: Given the high gross margins, lower seasonality, and scalable nature of the Intelligence platform, success in this segment can be measured simply: are we growing ARR as we maintain gross margin? If the answer to the first question is yes, then the top of the funnel is working well. We then ask how we are doing at delivering value to existing customers, which is where the NRR metric becomes relevant. To do all of this well requires a productized delivery model where incremental costs scale materially slower than revenue. As such, we must maintain discipline around product standardization, compute efficiency, and support scalability to preserve high incremental margins. Monitoring gross margins and, to a lesser extent at this stage of the product’s lifecycle, EBITDA margin will ensure that new revenue is added efficiently as we scale.

In summary, these metrics give investors the clearest picture of what we believe matter most. We will continue to answer questions about legacy metrics or topics of investor interest, but if an investor wants to understand how to model Triumph and how we are driving future value creation, I suggest focusing on these things.

Payments

1.Analysis of Financial and Operational Performance for the Quarter

2.Revenue Drivers and Growth Forecast

3.LoadPay Update

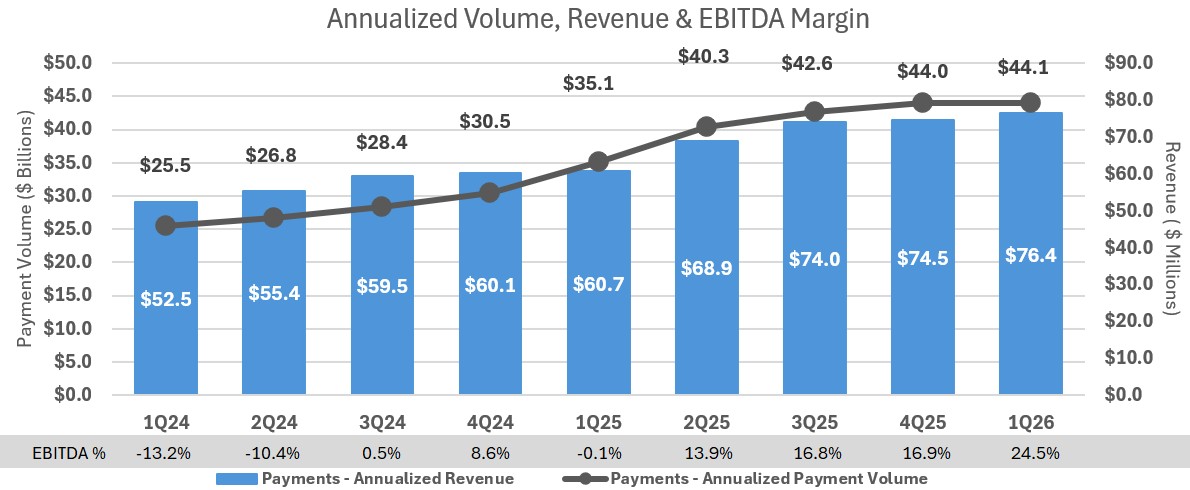

Analysis of Financial and Operational Performance for the Quarter. Revenue grew 2.6% QoQ despite a seasonal decline in invoice volumes of 9.2%. Fee and financing revenue grew 6.0% and 3.3%, respectively, partially offset by lower float revenue, which is correlated to the interest rate environment. Total revenue grew 25.8% YoY to $76.4 million, annualized. EBITDA margin for the quarter improved to 24.5%, up from (0.1)% in 1Q 2025. Ex-LoadPay, EBITDA margin for the quarter was 34.0%, up from 29.5% in 4Q 2025. Pretax operating income was $1.9 million.

3

| March 31, 2026 | December 31, 2025 | September 30, 2025 | June 30, 2025 | March 31, 2025 | Current Quarter Q/Q | Current Year Y/Y | |||||||||||||||||||||||||||||||||||||||||||||||

| For the Qtr Ending | Change | % Change | Change | % Change | |||||||||||||||||||||||||||||||||||||||||||||||||

| Payments: | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Invoice Volume | 8,220,371 | 9,053,274 | 8,826,848 | 8,500,565 | 7,182,044 | (832,903) | (9.2) | % | 1,038,327 | 14.5 | % | ||||||||||||||||||||||||||||||||||||||||||

| Payment Volume | $ | 11,014,040,000 | $ | 10,995,478,000 | $ | 10,662,418,000 | $ | 10,081,206,000 | $ | 8,777,825,000 | $ | 18,562,000 | 0.2 | % | $ | 2,236,215,000 | 25.5 | % | |||||||||||||||||||||||||||||||||||

Network Engagement[2] | 66.1 | % | 64.2 | % | 63.4 | % | 63.3 | % | 50.4 | % | 1.9 | % | 3.0 | % | 15.7 | % | 31.2 | % | |||||||||||||||||||||||||||||||||||

| Average Float | $ | 538,303,000 | $ | 518,182,000 | $ | 484,582,000 | $ | 469,211,000 | $ | 442,901,000 | $ | 20,121,000 | 3.9 | % | $ | 95,402,000 | 21.5 | % | |||||||||||||||||||||||||||||||||||

| Fee Revenue | $ | 9,450,000 | $ | 8,913,000 | $ | 8,791,000 | $ | 8,105,000 | $ | 6,903,000 | $ | 537,000 | 6.0 | % | $ | 2,547,000 | 36.9 | % | |||||||||||||||||||||||||||||||||||

| Total Revenue | $ | 19,104,000 | $ | 18,628,000 | $ | 18,503,000 | $ | 17,231,000 | $ | 15,184,000 | $ | 476,000 | 2.6 | % | $ | 3,920,000 | 25.8 | % | |||||||||||||||||||||||||||||||||||

| EBITDA margin | 24.5 | % | 16.9 | % | 16.8 | % | 13.9 | % | (0.1) | % | 7.6 | % | 45.0 | % | 24.6 | % | (24600.0) | % | |||||||||||||||||||||||||||||||||||

| EBITDA Margin (ex-LoadPay) | 34.0 | % | 29.5 | % | 28.2 | % | 22.7 | % | 5.9 | % | 4.5 | % | 15.3 | % | 28.1 | % | 476.3 | % | |||||||||||||||||||||||||||||||||||

| LoadPay: | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| # of Accounts | 8,065 | 5,892 | 4,421 | 2,367 | 778 | 2,173 | 36.9 | % | 7,287 | 936.6 | % | ||||||||||||||||||||||||||||||||||||||||||

| # of Active Carrier Accounts | 3,157 | 2,487 | 1,916 | 968 | 379 | 670 | 26.9 | % | 2,778 | 733.0 | % | ||||||||||||||||||||||||||||||||||||||||||

| Revenue per Account (Ann.) | $ | 252.21 | $ | 248.33 | $ | 234.70 | $ | 206.30 | $ | 200.93 | $3.88 | 1.6 | % | $51.28 | 25.5 | % | |||||||||||||||||||||||||||||||||||||

| Revenue per Active Carrier Account (Ann.) | $ | 633.10 | $ | 572.15 | $ | 516.78 | $ | 478.32 | $ | 393.82 | $60.95 | 10.7 | % | $239.28 | 60.8 | % | |||||||||||||||||||||||||||||||||||||

| LoadPay Funding | $ | 118,384,000 | $ | 84,770,000 | $ | 53,042,000 | $ | 22,212,000 | $ | 4,986,000 | $ | 33,614,000 | 39.7 | % | $ | 113,398,000 | 2274.3 | % | |||||||||||||||||||||||||||||||||||

| Average Interchange Fees | 1.62 | % | 1.68 | % | 1.64 | % | 1.61 | % | 1.76 | % | (0.06) | % | (3.6) | % | (0.1) | % | (5.7) | % | |||||||||||||||||||||||||||||||||||

| Cross Segment: | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Unique Broker Invoice Volume* | 9,994,137 | 10,689,056 | 10,689,315 | 10,217,761 | 9,353,366 | (694,919) | (6.5) | % | 640,771 | 6.9 | % | ||||||||||||||||||||||||||||||||||||||||||

| Broker Revenue* | $ | 13,056,000 | $ | 12,436,000 | $ | 12,343,000 | $ | 10,985,000 | $ | 8,241,000 | $ | 620,000 | 5.0 | % | $4,815,000 | 58.4 | % | ||||||||||||||||||||||||||||||||||||

| Broker Revenue Per Invoice | $ | 1.31 | $ | 1.16 | $ | 1.15 | $ | 1.08 | $ | 0.88 | $0.15 | 12.9 | % | $0.43 | 48.9 | % | |||||||||||||||||||||||||||||||||||||

| PAR | 1.30 | 1.33 | 1.31 | 1.30 | 1.24 | (0.03) | (2.3) | % | 0.06 | 4.8 | % | ||||||||||||||||||||||||||||||||||||||||||

* Unique Broker Invoice Volume refers to Invoices from our broker Payments and Audit services as well as our Intelligence services to brokers.

* Broker Revenue is the revenue generated by our broker Payments and Audit services (Broker Fee Income + Quickpay Interest Income) + broker Intelligence revenue.

For 1Q 2026, the dollar-volume of Payments was flat as the seasonal decline in invoice volume was offset by increasing invoice prices. It is worth highlighting that Payments services are generally charged on a per invoice basis, so invoice counts are a better gauge of revenue growth than Payments volumes.

In the chart below, we graphically highlight the continued revenue growth and its trend over the last eight quarters against the backdrop of our Payment volumes. We have generated a ~21% CAGR in revenue over the last two years despite the continuance of the longest recession in the history of trucking.

4

Revenue Drivers and Growth Forecast. Payments revenue growth is driven by three levers: winning net new relationships, deepening existing ones, and value-based pricing. Repricing was the largest growth driver in the quarter, but we also brought on and ramped up several new relationships while deepening relationships with others through our cross-selling efforts. The second phase of our contractual repricing efforts went into effect on April 1. There will be an additional phase on July 1. By 4Q 2026, we expect over $10 million of incremental annualized revenue from our repricing efforts.

As highlighted above, we are introducing revenue per invoice and our PAR to assist investors in monitoring our progress. Revenue per invoice grew to $1.31, an increase of $0.15 (12.9%) from 4Q 2025. PAR was 1.30. Cross-selling represents significant upside and is a compounding lever to drive continued growth in revenue per invoice.

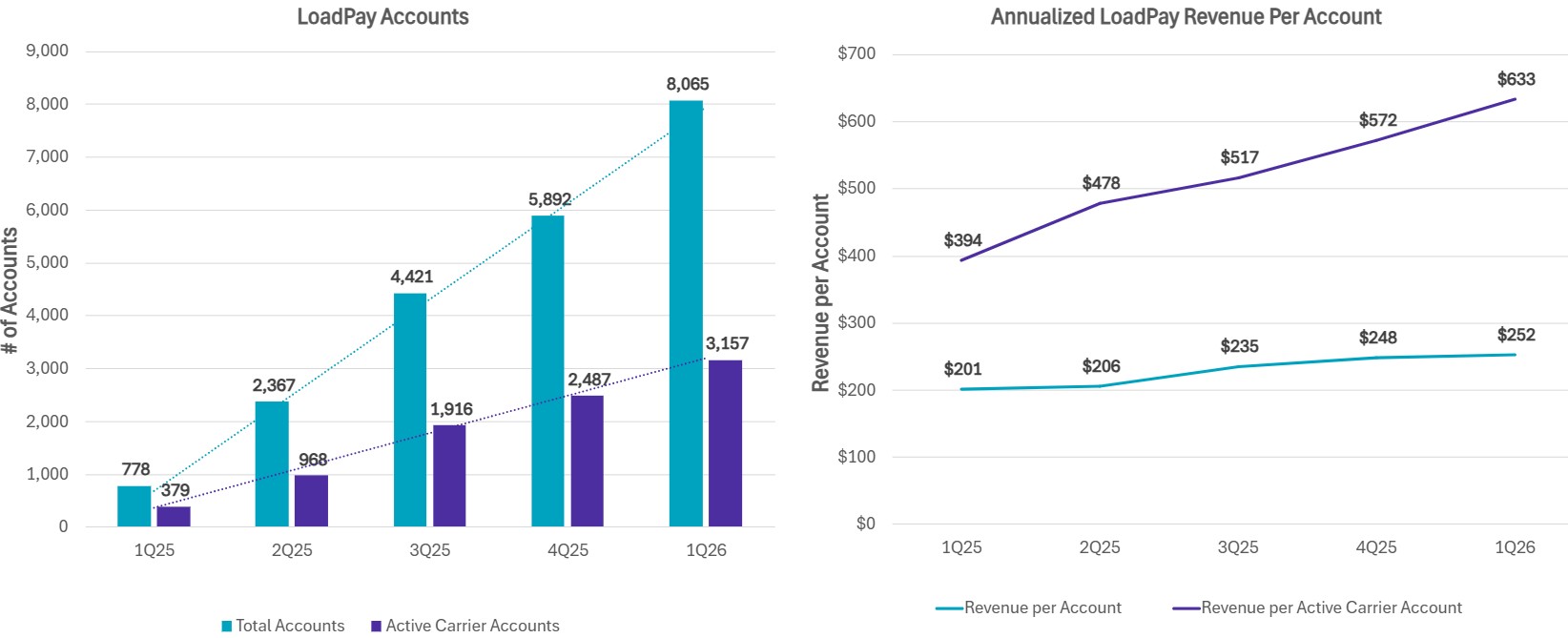

LoadPay Update. LoadPay remains an early-stage product inside our Payments segment. We continue to focus on growth in accounts and the revenue per active carrier account. For the quarter, gross revenue was $437 thousand, revenue per account was $252, and revenue per active carrier account was $633. As a reminder, our target annual revenue for active carrier accounts is $750. That number was an estimate we calculated at the time we introduced LoadPay. I am hopeful that as we introduce more features over time, that estimate proves to be materially below the opportunity threshold. For the quarter, the percentage of accounts active was 39.1% of all accounts, and the total number of accounts was 8,065. In the chart below, we graphically highlight these elements over the last five quarters.

Factoring

1.Analysis of Financial and Operational Performance for the Quarter

2.Automation and AI Update

Analysis of Financial and Operational Performance for the Quarter. The Factoring segment delivered pretax operating income of $14.5 million. Revenue decreased (0.4)% QoQ, and pretax operating margin was 34.7%. Total purchased volume reached $3.3 billion for the quarter, a 4.6% increase over 4Q 2025, and 20.5% over the same quarter in 2025. That is robust growth for a mature business. I am also impressed with how our team outperformed seasonality in the first quarter. Our Payments business, which is a reasonable proxy for the industry, saw a 9.2% decline in invoice volumes in 1Q 2026 due to seasonality. Our Factoring invoice volumes declined 3.5% in the same period, which was ~2/3 less than the Payments decline. This positive variance illustrates our growth in market share.

5

| March 31, 2026 | December 31, 2025 | September 30, 2025 | June 30, 2025 | March 31, 2025 | Current Quarter Q/Q | Current Year Y/Y | |||||||||||||||||||||||||||||||||||||||||||||||

| For the Qtr Ending | Change | % Change | Change | % Change | |||||||||||||||||||||||||||||||||||||||||||||||||

| Factoring: | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Invoice Volume | 1,683,160 | 1,744,811 | 1,735,860 | 1,697,851 | 1,497,644 | (61,651) | (3.5) | % | 185,516 | 12.4 | % | ||||||||||||||||||||||||||||||||||||||||||

| Purchased Volume | $ | 3,262,610,000 | $ | 3,119,443,000 | $ | 2,997,895,000 | $ | 2,873,659,000 | $ | 2,707,805,000 | $ | 143,167,000 | 4.6 | % | $ | 554,805,000 | 20.5 | % | |||||||||||||||||||||||||||||||||||

| Average Transportation Invoice Size | $ | 1,897 | $ | 1,751 | $ | 1,690 | $ | 1,663 | $ | 1,769 | $ | 146 | 8.3 | % | $ | 128 | 7.2 | % | |||||||||||||||||||||||||||||||||||

| Invoices / Client | 226 | 241 | 236 | 232 | 204 | (15) | (6.2) | % | 22 | 10.8 | % | ||||||||||||||||||||||||||||||||||||||||||

| Discount Rate | 1.28 | % | 1.28 | % | 1.29 | % | 1.37 | % | 1.31 | % | — | % | — | % | (0.03) | % | (2.3) | % | |||||||||||||||||||||||||||||||||||

| Avg Daily Purchases* | $ | 53,485,000 | $ | 50,314,000 | $ | 46,842,000 | $ | 45,614,000 | $ | 44,390,000 | 3,171,000 | 6.3 | % | 9,095,000 | 20.5 | % | |||||||||||||||||||||||||||||||||||||

| # of Customers | 7,436 | 7,241 | 7,355 | 7,319 | 7,352 | 195 | 2.7 | % | 84 | 1.1 | % | ||||||||||||||||||||||||||||||||||||||||||

| PAR | 1.19 | 1.17 | 1.16 | 1.12 | 1.09 | 0.02 | 1.7 | % | 0.10 | 9.2 | % | ||||||||||||||||||||||||||||||||||||||||||

| Operating margin | 34.72 | % | 32.61 | % | 20.71 | % | 48.46 | % | 19.24 | % | 2.11 | % | 6.5 | % | 15.48 | % | 80.5 | % | |||||||||||||||||||||||||||||||||||

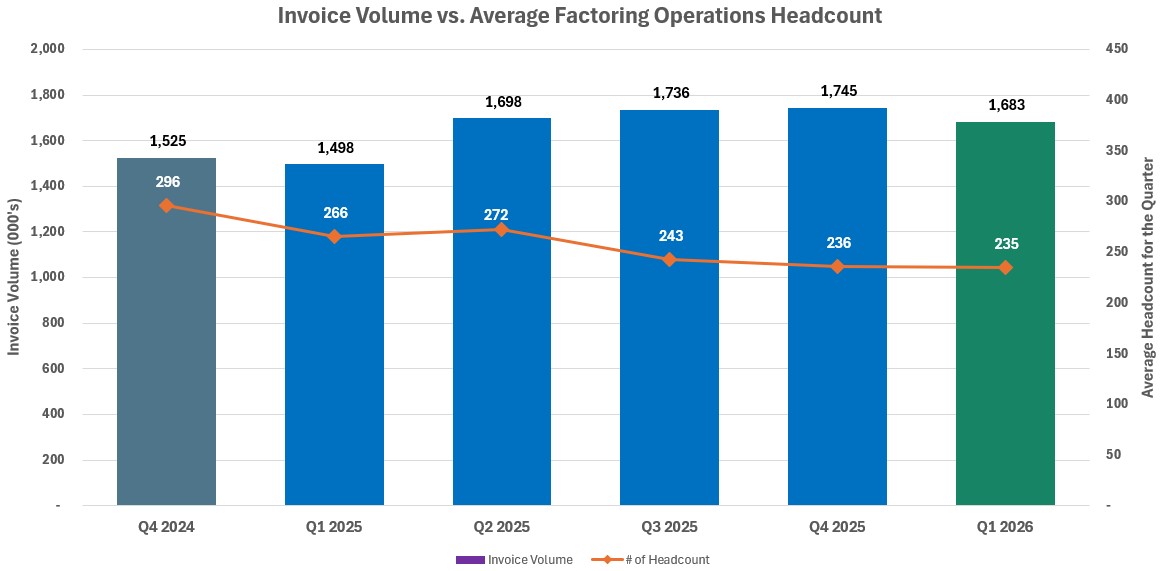

Automation and AI Update. Our instant decision platform continues to drive meaningful operating leverage. During the quarter, we purchased approximately 1.7 million invoices supported by 235 average full‑time employees, representing a 12.4% increase in the number of invoices purchased by 11.4% fewer FTEs compared to the same quarter last year. This improvement reflects the scalability of our operating model and our ability to support higher transaction volumes without proportional increases in headcount. These gains are being reinforced by broader efficiency gains across Factoring. We are simplifying workflows, reducing handoffs, and eliminating non‑value‑added activities which results in measurable improvements in both capacity and operating margin.

In parallel, we are advancing a focused set of AI‑ and LLM‑enabled automation initiatives alongside pragmatic process simplification across decisioning, cash application, and collections. While several initiatives remain in progress, early results are translating into improved throughput and workflow efficiency, supporting continued increases in invoices processed per employee. These efforts are strengthening the scalability of our operating model, enabling us to support growth without proportional cost expansion, with the benefits reflected in our expense outlook. As these initiatives mature, we expect further efficiency gains and sustained margin support as volumes scale.

Last quarter, we introduced a chart comparing client-facing headcount with the number of invoices purchased, highlighting meaningful efficiency gains from our investments. Going forward, as AI and automation extend beyond the back office to encompass the entire factoring operation, we will continue to demonstrate these efficiencies across the business.

6

Intelligence

1.Analysis of Financial and Operational Performance for the Quarter

2.Our Focus in 2026

3.How Triumph Intelligence is Different

Analysis of Financial and Operational Performance for the Quarter. Intelligence revenue was $2.4 million, up 2.1% QoQ, while gross margin was 86%. We continue to expect 2026 revenue in this business to increase materially.

| March 31, 2026 | December 31, 2025 | September 30, 2025 | June 30, 2025 | March 31, 2025 | Current Quarter Q/Q | Current Year Y/Y | |||||||||||||||||||||||||||||||||||||||||||||||

| For the Qtr Ending | Change | % Change | Change | % Change | |||||||||||||||||||||||||||||||||||||||||||||||||

| Intelligence: | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Annual Recurring Revenue (ARR) | $ | 8,445,963 | $ | 8,297,772 | $ | 8,306,590 | $ | 8,045,118 | $ | 8,003,372 | $ | 148,191 | 1.8 | % | $ | 442,591 | 5.5 | % | |||||||||||||||||||||||||||||||||||

| Net Revenue Retention (NRR) | 93.4 | % | 94.1 | % | 98.8 | % | 95.2 | % | 98.0 | % | (0.7) | % | (0.7) | % | (4.6) | % | (4.7) | % | |||||||||||||||||||||||||||||||||||

| EBITDA Margin | (68.7) | % | (42.2) | % | (94.6) | % | n/m | n/m | (26.5) | % | 62.8 | % | n/m | n/m | |||||||||||||||||||||||||||||||||||||||

Our Focus in 2026. This year, the focus will be on growing PAR through cross-selling and a more robust Intelligence platform that brings together all constituents in the ecosystem with an emphasis on enabling sustainable, strategic relationships through Capacity Intelligence and support for RFP collaboration. We are also adding additional Intelligence tools aimed at enterprise brokers who have already made investments in data science in their own organizations. Capacity Intelligence is a strategic engine inside Triumph Intelligence that helps capacity teams build predictable, profitable, relationship-based carrier networks. It identifies the lanes that matter most, surfaces the right carriers to serve them and guides teams through a simple, repeatable workflow. Capacity Intelligence is not a load board or an exchange, nor is it designed to replace either. Capacity Intelligence solves a different challenge: providing a means for brokers to identify lanes within their networks where optimizing non-transactional freight will result in more stability.

How Triumph Intelligence Is Different. Triumph Intelligence is the only scaled market intelligence provider that delivers a holistic market price, considering performance and capacity, on both the buy and sell side of the broker transaction. We believe our offering is superior to incumbents not only because we have “more features,” but because we have better data, better analytics, and a forward-looking posture. Fully settled real-time transactions are THE best source of truth. This data set allows machine learning to build firm-specific views which create realizable value for customers. As we continue to integrate Intelligence into the Triumph Network, we expect a reinforcing feedback loop: adoption in other segments enriches the data asset, thereby increasing product value for those same customers.

Freight Market Analysis

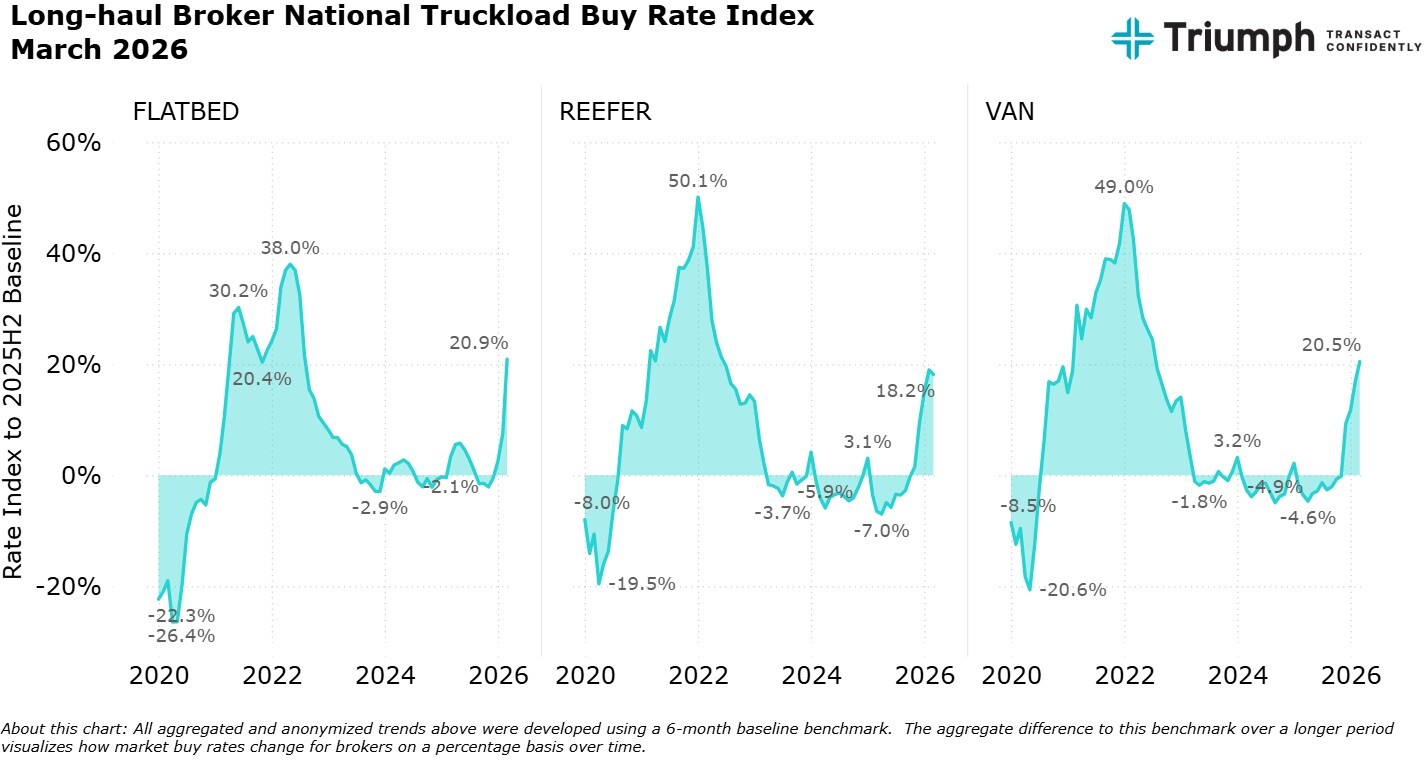

The following observations reflect transaction-backed insights from the Triumph Network, offering a real-time perspective on market dynamics. The first quarter of 2026 exhibited a significant continuation of rate inflation first measured in December 2025 across all transport types driven by fuel prices, improvements in demand, and continued non-domiciled CDL supply-related driver reductions.

The Triumph Network supports five key findings for 1Q 2026:

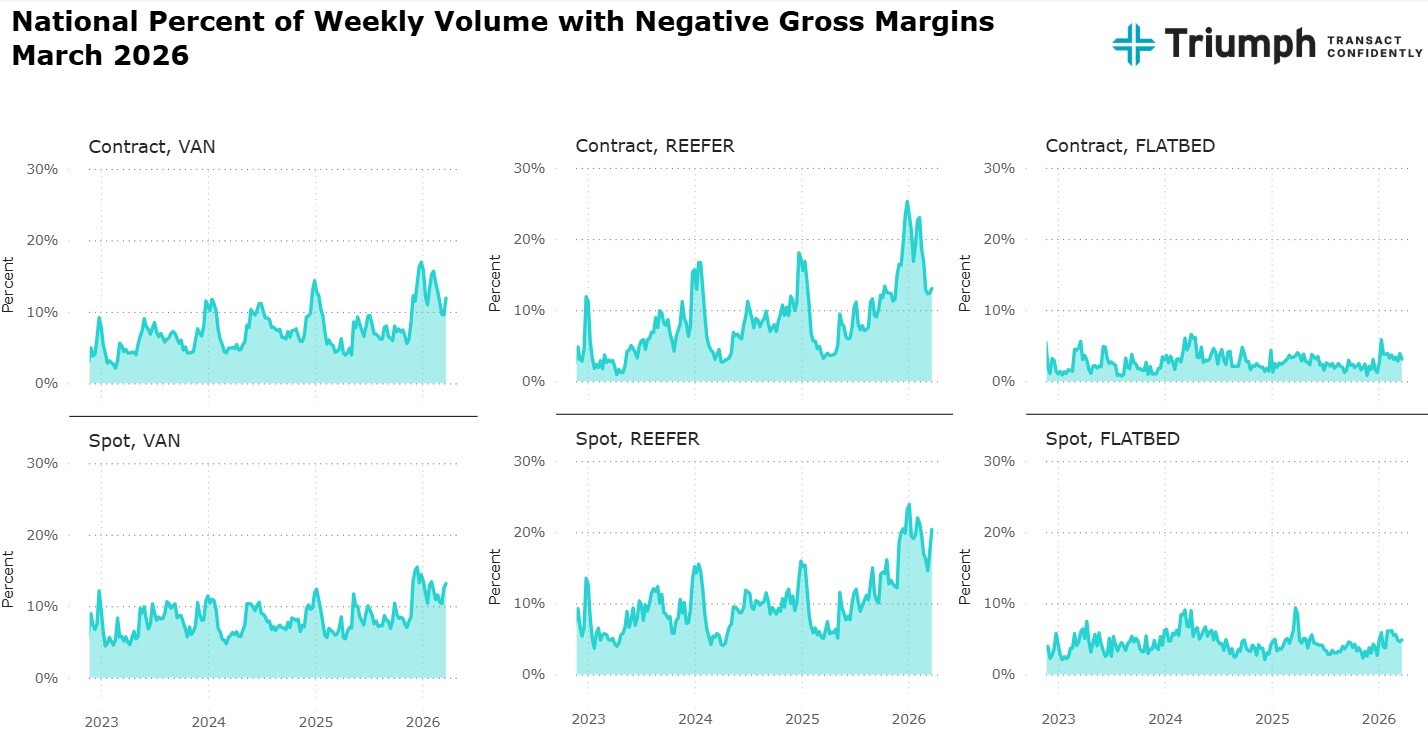

1.Negative weekly gross margin volume trended above 10% for most weeks across Van and Reefer freight volumes, with four weeks measuring above 20% for Reefer. These figures exceed all prior post-Covid markets. (Chart below: National Percent of Weekly Volume with Negative Margins)

2.Aggregate rate inflation rates over the last four months met or exceeded month-over-month (MoM) inflation rates witnessed during Covid. However, current truckload pricing is consistently within levels experienced in 1Q 2021, which was 12-months shy of peak Covid rate inflation occurring in 1Q 2022. (Chart below: Long-haul Broker National Truckload Buy Rate Index)

3.Flatbed, which is typically affected by lower seasonal demand, showed significant rate inflation in March exceeding all measured MoM rates of inflation of any transport type since pre-Covid at 13.4% MoM. While exact causality is unattainable, data center construction combined with higher fuel prices is a likely driver of this anomalous rate inflation. (Chart below: Long-haul Broker National Truckload Buy Rate Index)

7

4.The Iran conflict has increased fuel rates almost $2 per gallon over 1Q 2026. Carriers will experience an estimated 30-40 cents per mile increase in fuel expense as a result, significantly adding costs to fleets with higher empty miles figures across their networks. Fleets struggling with higher operating ratios will certainly feel more pressure from this key input cost.

5.Industrial and manufacturing-related demand are showing signs of improvement. The ISM PMI Composite Index, a key forward indicator of trucking demand, has maintained expansion level readings for all months in 1Q 2026.

Looking Ahead

Much of what we reported last quarter is still in play — rate inflation, margin compression, and CDL enforcement. Visibility to these issues is growing beyond transportation industry actors. Key rulings from the Supreme Court this summer, as well as continued administrative policy changes from FMCSA/DOT, are the biggest questions the transportation industry faces this year. Any significant changes to the levels of liability or driver certification requirements could recast the trucking industry significantly, adding bottlenecks to fleet expansion or additional administrative requirements across industry actors in an already challenged marketplace.

8

Banking

1.Analysis of Financial and Operational Performance for the Quarter

2.Update on Credit Metrics

3.Portfolio Simplification

Analysis of Financial and Operational Performance for the Quarter. Banking segment operating income decreased $1.0 million to $24.6 million, or 3.9%, from the prior quarter, driven by lower average loan balances as well as lower interest rates. During the quarter, we added roughly $1 billion of new servicing deposits from mortgage warehouse clients. As a result of these deposits, cash balances increased and wholesale funding such as FHLB advances and brokered deposits declined.

Update on Credit Metrics. The metrics reflect credit exposure work tied to some of the business lines we are exiting, as well as normal-course credit noise. We continue to monitor the bankruptcy proceedings related to our Tricolor ABL exposure, and we continue to believe that our loan position is adequately secured by inventory and other assets that serve as our collateral.

•Total non-performing loans to total loans: increased by 0.62% to 1.77% due primarily to one large classified CRE loan that was moved to nonaccrual during the quarter. We completed an appraisal in March that indicates no reserve is warranted at this time.

•Total classified assets: decreased by ~$3.3 million to $184.0 million.

•Past due to total loans: decreased by 0.37% to 2.35% due primarily to improving credit trends in equipment finance and lower past due balances in factoring.

Portfolio Simplification. Our banking team is focused on generating and maintaining a healthy, low-cost funding base through excellent service and competitive products in the communities we serve. Our national lending businesses continue to empower their customers through mortgage warehouse services, temporary and short-term real estate financing, and equipment lending. We continue to expect loan growth in total to be flat for the overall company in 2026 as growth in factored receivables is offset by declines in our ABL and liquid credit portfolios and other strategic opportunities in the Banking segment’s portfolio.

9

AI, Disruption, and Our Approach

We generally think about AI in three categories: functionality, efficiency, and data. We participate in all three. Investors may see the data and product opportunity today; the efficiency benefits should be increasingly visible in 2026.

Our working view is that AI will compress “feature moats” across software, but it does not eliminate moats built on trusted networks, embedded workflows, and proprietary real‑time data. The most useful way to frame this — internally and with investors — is to distinguish between building a tool and operating a two‑sided network that sits inside the core transaction. In that construct, AI may replicate discrete product functionality faster, but it cannot reproduce the combination of network participation on both sides of the freight payment, the trust layer that enables audit and accurate settlement, the fraud‑mitigation guardrails, and the downstream intelligence embedded within those workflows. The defensibility is therefore less about “software we wrote” and more about the ecosystem we operate and the data asset we continuously create: settled, clean, real‑time transactions that can train models and drive actionable intelligence in a high‑confidence environment.

At the operating level, we view AI as both (i) a lever to lower cost‑to‑serve and (ii) an opportunity to redesign workflows from first principles rather than simply “bolting AI on” to existing processes. The strategic winners will be the companies that rebuild processes around AI and use it to do things better and differently — not just faster. We are applying that mindset alongside a lean operating posture that remains customer‑centric and innovation‑forward, while maintaining humility about the range of outcomes and resisting hype-driven narratives. We expect to continue innovating as we execute, with outcomes investors can see in our results, not press releases.

Expense Forecast and Closing Thoughts

We project expenses of $97.0 million for 2Q 2026. We are grateful for the interest investors have shown in Triumph and for the patience many have demonstrated as we invested through the cycle. Our responsibility now is to reward that patience with consistent, high-margin revenue growth and earnings growth. If we do those things, with an eye fixed firmly on the North Star framework — compounding transportation revenue and steadily improving margins — we believe the results will take care of themselves.

With warm regards,

Aaron P. Graft

Founder, Vice Chairman and CEO

[1] The Rule of 40 recognizes that young companies trade profit today for growth tomorrow, while mature companies generate cash even if growth slows. A rule of 40 business is healthy, investable, and speaks to viability. A rule of 60 business is best in class and speaks to quality and durability.

[2] We define Network engagement as the amount of freight touched through our payments, audit, full AP automation and rate intelligence products. It is an indicator of our broker volume density in the market, the source for growing available Network transactions and data assets, and a key value driver of the Network.

10

Conference Call Information

Aaron P. Graft, Vice Chairman and CEO, and Brad Voss, CFO, will review the financial results in a conference call with investors and analysts beginning at 9:30 a.m. central time on Wednesday, April 22, 2026.

The live video conference may be accessed directly through this link, https://triumph-financial-q1-2026-earnings.open-exchange.net/ or via the Company's IR website at ir.triumph.io through the Financial Results link. An archive of this video conference will subsequently be available at the same location, referenced above, on the Company’s website.

About Triumph Financial

Triumph Financial, Inc. (NYSE: TFIN) is a financial and technology company focused on payments, factoring, intelligence and banking to modernize and simplify freight transactions. Headquartered in Dallas, Texas, its portfolio of brands includes Triumph, TBK Bank and LoadPay. ir.triumph.io

Forward-Looking Statements

This letter to shareholders contains forward-looking statements. Any statements about our expectations, beliefs, plans, predictions, forecasts, objectives, assumptions or future events or performance are not historical facts and may be forward-looking. You can identify forward-looking statements by the use of forward-looking terminology such as “believes,” “expects,” “could,” “may,” “will,” “should,” “seeks,” “likely,” “intends,” “plans,” “pro forma,” “projects,” “estimates” or “anticipates” or the negative of these words and phrases or similar words or phrases that are predictions of or indicate future events or trends and that do not relate solely to historical matters. You can also identify forward-looking statements by discussions of strategy, plans or intentions. Forward-looking statements involve numerous risks and uncertainties, and you should not rely on them as predictions of future events. Forward-looking statements depend on assumptions, data or methods that may be incorrect or imprecise and we may not be able to realize them. We do not guarantee that the transactions and events described will happen as described (or that they will happen at all). The following factors, among others, could cause actual results and future events to differ materially from those set forth or contemplated in the forward-looking statements: business and economic conditions generally and in the bank and non-bank financial services industries, nationally and within our local market areas; our ability to mitigate our risk exposures; our ability to maintain our historical earnings trends; changes in management personnel; interest rate risk; concentration of our products and services in the transportation industry; credit risk associated with our loan portfolio; lack of seasoning in our loan portfolio; deteriorating asset quality and higher loan charge-offs; time and effort necessary to resolve non-performing assets; inaccuracy of the assumptions and estimates we make in establishing reserves for probable loan losses and other estimates; risks related to the integration of acquired businesses and any future acquisitions; our ability to successfully identify and address the risks associated with our possible future acquisitions, and the risks that our prior and possible future acquisitions make it more difficult for investors to evaluate our business, financial condition and results of operations, and impairs our ability to accurately forecast our future performance; lack of liquidity; fluctuations in the fair value and liquidity of the securities we hold for sale; impairment of investment securities, goodwill, other intangible assets or deferred tax assets; our risk management strategies; environmental liability associated with our lending activities; increased competition in the bank and non-bank financial services industries, nationally, regionally or locally, which may adversely affect pricing and terms; the accuracy of our financial statements and related disclosures; material weaknesses in our internal control over financial reporting; system failures or failures to prevent breaches of our network security; the institution and outcome of litigation and other legal proceedings against us or to which we become subject; changes in carry-forwards of net operating losses; changes in federal tax law or policy; the impact of recent and future legislative and regulatory changes, including changes in banking, securities and tax laws and regulations, such as the Dodd-Frank Act and their application by our regulators as well as privacy, cybersecurity, and artificial intelligence regulation and oversight; governmental monetary and fiscal policies; changes in the scope and cost of FDIC, insurance and other coverages; failure to receive regulatory approval for future acquisitions and increases in our capital requirements.

11

While forward-looking statements reflect our good-faith beliefs, they are not guarantees of future performance. All forward-looking statements are necessarily only estimates of future results. Accordingly, actual results may differ materially from those expressed in or contemplated by the particular forward-looking statement, and, therefore, you are cautioned not to place undue reliance on such statements. Further, any forward-looking statement speaks only as of the date on which it is made, and we undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events or circumstances, except as required by applicable law. For a discussion of such risks and uncertainties, which could cause actual results to differ from those contained in the forward-looking statements, see "Risk Factors" and the forward-looking statement disclosure contained in Triumph Financial’s Annual Report on Form 10-K, filed with the Securities and Exchange Commission on February 11, 2026.

Non-GAAP Financial Measures

This letter to shareholders includes certain non‐GAAP financial measures intended to supplement, not substitute for, comparable GAAP measures. Reconciliations of non‐GAAP financial measures to GAAP financial measures are provided at the end of this letter to shareholders.

12

The following table sets forth key metrics used by Triumph Financial to monitor our operations. Footnotes in this table can be found in our definitions of non-GAAP financial measures at the end of this document.

| As of and for the Three Months Ended | |||||||||||||||||||||||||||||

| (Dollars in thousands) | March 31, 2026 | December 31, 2025 | September 30, 2025 | June 30, 2025 | March 31, 2025 | ||||||||||||||||||||||||

| Financial Highlights: | |||||||||||||||||||||||||||||

| Total assets | $ | 6,876,715 | $ | 6,380,588 | $ | 6,357,149 | $ | 6,494,748 | $ | 6,268,394 | |||||||||||||||||||

| Loans held for investment | $ | 5,189,139 | $ | 4,991,307 | $ | 4,986,922 | $ | 4,953,170 | $ | 4,666,223 | |||||||||||||||||||

| Deposits | $ | 5,699,939 | $ | 4,950,216 | $ | 4,955,246 | $ | 5,186,098 | $ | 4,976,750 | |||||||||||||||||||

| Net income available to common stockholders | $ | 5,554 | $ | 18,412 | $ | 907 | $ | 3,618 | $ | (784) | |||||||||||||||||||

| Performance Ratios - Annualized: | |||||||||||||||||||||||||||||

| Return on average assets | 0.39 | % | 1.18 | % | 0.11 | % | 0.28 | % | — | % | |||||||||||||||||||

| Return on average total equity | 2.71 | % | 8.14 | % | 0.73 | % | 1.95 | % | 0.01 | % | |||||||||||||||||||

| Return on average common equity | 2.48 | % | 8.19 | % | 0.41 | % | 1.68 | % | (0.37 | %) | |||||||||||||||||||

Return on average tangible common equity (1) | 4.46 | % | 15.00 | % | 0.76 | % | 2.81 | % | (0.53 | %) | |||||||||||||||||||

| Yield on loans | 7.72 | % | 8.14 | % | 8.17 | % | 8.41 | % | 8.37 | % | |||||||||||||||||||

| Cost of interest bearing deposits | 2.07 | % | 2.28 | % | 2.36 | % | 2.22 | % | 2.14 | % | |||||||||||||||||||

| Cost of total deposits | 1.07 | % | 1.29 | % | 1.35 | % | 1.25 | % | 1.23 | % | |||||||||||||||||||

| Cost of total funds | 1.22 | % | 1.48 | % | 1.55 | % | 1.53 | % | 1.45 | % | |||||||||||||||||||

| Net interest margin | 6.06 | % | 6.36 | % | 6.29 | % | 6.43 | % | 6.49 | % | |||||||||||||||||||

Net noninterest expense to average assets(1) | 4.85 | % | 4.16 | % | 5.08 | % | 5.13 | % | 5.61 | % | |||||||||||||||||||

Asset Quality:(2) | |||||||||||||||||||||||||||||

| Past due to total loans | 2.35 | % | 2.72 | % | 1.91 | % | 2.21 | % | 3.24 | % | |||||||||||||||||||

| Non-performing loans to total loans | 1.77 | % | 1.15 | % | 1.36 | % | 1.20 | % | 2.07 | % | |||||||||||||||||||

| Non-performing assets to total assets | 1.53 | % | 1.10 | % | 1.10 | % | 1.04 | % | 1.64 | % | |||||||||||||||||||

| ACL to non-performing loans | 37.15 | % | 63.44 | % | 49.53 | % | 65.02 | % | 37.47 | % | |||||||||||||||||||

| ACL to total loans | 0.66 | % | 0.73 | % | 0.67 | % | 0.78 | % | 0.78 | % | |||||||||||||||||||

| Net charge-offs to average loans | 0.04 | % | (0.10 | %) | 0.19 | % | 0.17 | % | 0.13 | % | |||||||||||||||||||

| Capital: | |||||||||||||||||||||||||||||

Tier 1 capital to average assets(3) | 9.90 | % | 9.86 | % | 9.55 | % | 9.46 | % | 12.04 | % | |||||||||||||||||||

Tier 1 capital to risk-weighted assets(3) | 10.68 | % | 10.74 | % | 10.20 | % | 9.98 | % | 12.90 | % | |||||||||||||||||||

Common equity tier 1 capital to risk-weighted assets(3) | 9.14 | % | 9.16 | % | 8.65 | % | 8.43 | % | 11.27 | % | |||||||||||||||||||

Total capital to risk-weighted assets(3) | 12.56 | % | 12.71 | % | 12.09 | % | 11.95 | % | 14.93 | % | |||||||||||||||||||

| Total equity to total assets | 13.83 | % | 14.76 | % | 14.46 | % | 14.05 | % | 14.26 | % | |||||||||||||||||||

Tangible common stockholders' equity to tangible assets(1) | 7.80 | % | 8.26 | % | 7.87 | % | 7.53 | % | 9.86 | % | |||||||||||||||||||

| Per Share Amounts: | |||||||||||||||||||||||||||||

| Book value per share | $ | 38.05 | $ | 37.73 | $ | 36.79 | $ | 36.56 | $ | 36.25 | |||||||||||||||||||

Tangible book value per share (1) | $ | 21.21 | $ | 20.77 | $ | 19.70 | $ | 19.31 | $ | 25.32 | |||||||||||||||||||

| Basic earnings per common share | $ | 0.23 | $ | 0.77 | $ | 0.04 | $ | 0.15 | $ | (0.03) | |||||||||||||||||||

| Diluted earnings per common share | $ | 0.23 | $ | 0.77 | $ | 0.04 | $ | 0.15 | $ | (0.03) | |||||||||||||||||||

| Shares outstanding end of period | 23,806,253 | 23,765,385 | 23,763,401 | 23,727,046 | 23,419,740 | ||||||||||||||||||||||||

13

Unaudited consolidated balance sheet as of:

| (Dollars in thousands) | March 31, 2026 | December 31, 2025 | September 30, 2025 | June 30, 2025 | March 31, 2025 | ||||||||||||||||||||||||

| ASSETS | |||||||||||||||||||||||||||||

| Total cash and cash equivalents | $ | 581,939 | $ | 248,471 | $ | 147,222 | $ | 282,346 | $ | 502,944 | |||||||||||||||||||

| Securities - available for sale | 339,562 | 364,277 | 378,088 | 392,275 | 411,925 | ||||||||||||||||||||||||

| Securities - held to maturity, net | 1,031 | 1,550 | 1,766 | 1,782 | 1,731 | ||||||||||||||||||||||||

| Equity securities with readily determinable fair value | 4,559 | 4,588 | 4,569 | 4,526 | 4,512 | ||||||||||||||||||||||||

| Loans held for sale | 2,495 | 459 | 9,741 | 6,066 | 2,950 | ||||||||||||||||||||||||

| Loans held for investment | 5,189,139 | 4,991,307 | 4,986,922 | 4,953,170 | 4,666,223 | ||||||||||||||||||||||||

| Allowance for credit losses | (34,157) | (36,511) | (33,549) | (38,691) | (36,229) | ||||||||||||||||||||||||

| Loans, net | 5,154,982 | 4,954,796 | 4,953,373 | 4,914,479 | 4,629,994 | ||||||||||||||||||||||||

| FHLB and other restricted stock | 4,366 | 14,253 | 14,092 | 13,339 | 12,987 | ||||||||||||||||||||||||

| Premises and equipment, net | 89,492 | 91,071 | 141,141 | 149,120 | 150,247 | ||||||||||||||||||||||||

| Capitalized software, net | 48,322 | 46,370 | 44,934 | 43,011 | 40,869 | ||||||||||||||||||||||||

| Goodwill | 355,296 | 355,296 | 353,898 | 353,900 | 241,949 | ||||||||||||||||||||||||

| Intangible assets, net | 45,372 | 47,888 | 52,291 | 55,265 | 13,963 | ||||||||||||||||||||||||

| Bank-owned life insurance | 65,406 | 64,887 | 64,338 | 63,787 | 63,200 | ||||||||||||||||||||||||

| Deferred tax asset, net | — | 181 | — | 3,023 | 11,868 | ||||||||||||||||||||||||

| Other assets | 183,893 | 186,501 | 191,696 | 211,829 | 179,255 | ||||||||||||||||||||||||

| Total assets | $ | 6,876,715 | $ | 6,380,588 | $ | 6,357,149 | $ | 6,494,748 | $ | 6,268,394 | |||||||||||||||||||

| LIABILITIES | |||||||||||||||||||||||||||||

| Noninterest bearing deposits | $ | 3,042,210 | $ | 1,901,638 | $ | 2,095,017 | $ | 2,285,327 | $ | 2,260,048 | |||||||||||||||||||

| Interest bearing deposits | 2,657,729 | 3,048,578 | 2,860,229 | 2,900,771 | 2,716,702 | ||||||||||||||||||||||||

| Total deposits | 5,699,939 | 4,950,216 | 4,955,246 | 5,186,098 | 4,976,750 | ||||||||||||||||||||||||

| Federal Home Loan Bank advances | 30,000 | 280,000 | 280,000 | 180,000 | 205,000 | ||||||||||||||||||||||||

| Subordinated notes | 69,929 | 69,879 | 69,829 | 69,780 | 69,732 | ||||||||||||||||||||||||

| Junior subordinated debentures | 43,154 | 42,991 | 42,829 | 42,666 | 42,507 | ||||||||||||||||||||||||

| Deferred tax liabilities, net | 4,454 | — | 687 | — | — | ||||||||||||||||||||||||

| Other liabilities | 78,524 | 95,731 | 89,225 | 103,822 | 80,478 | ||||||||||||||||||||||||

| Total liabilities | 5,926,000 | 5,438,817 | 5,437,816 | 5,582,366 | 5,374,467 | ||||||||||||||||||||||||

| EQUITY | |||||||||||||||||||||||||||||

| Preferred Stock | 45,000 | 45,000 | 45,000 | 45,000 | 45,000 | ||||||||||||||||||||||||

| Common stock | 296 | 295 | 295 | 295 | 292 | ||||||||||||||||||||||||

| Additional paid-in-capital | 601,832 | 597,466 | 593,624 | 588,302 | 572,143 | ||||||||||||||||||||||||

| Treasury stock, at cost | (270,711) | (270,619) | (270,619) | (270,619) | (268,520) | ||||||||||||||||||||||||

| Retained earnings | 576,922 | 571,368 | 552,956 | 552,049 | 548,431 | ||||||||||||||||||||||||

| Accumulated other comprehensive income (loss) | (2,624) | (1,739) | (1,923) | (2,645) | (3,419) | ||||||||||||||||||||||||

| Total stockholders' equity | 950,715 | 941,771 | 919,333 | 912,382 | 893,927 | ||||||||||||||||||||||||

| Total liabilities and equity | $ | 6,876,715 | $ | 6,380,588 | $ | 6,357,149 | $ | 6,494,748 | $ | 6,268,394 | |||||||||||||||||||

14

Unaudited consolidated statement of income:

| For the Three Months Ended | |||||||||||||||||||||||||||||

| (Dollars in thousands) | March 31, 2026 | December 31, 2025 | September 30, 2025 | June 30, 2025 | March 31, 2025 | ||||||||||||||||||||||||

| Interest income: | |||||||||||||||||||||||||||||

| Loans, including fees | $ | 47,656 | $ | 55,233 | $ | 56,400 | $ | 54,836 | $ | 53,576 | |||||||||||||||||||

| Factored receivables, including fees | 46,021 | 46,165 | 43,841 | 44,217 | 38,694 | ||||||||||||||||||||||||

| Securities | 4,540 | 5,083 | 5,489 | 5,721 | 5,308 | ||||||||||||||||||||||||

| FHLB and other stock | 272 | 969 | 223 | 246 | 249 | ||||||||||||||||||||||||

| Cash deposits | 4,266 | 2,606 | 2,987 | 4,181 | 4,443 | ||||||||||||||||||||||||

| Total interest income | 102,755 | 110,056 | 108,940 | 109,201 | 102,270 | ||||||||||||||||||||||||

| Interest expense: | |||||||||||||||||||||||||||||

| Deposits | 14,052 | 16,639 | 17,532 | 15,505 | 14,397 | ||||||||||||||||||||||||

| Subordinated notes | 662 | 662 | 661 | 661 | 682 | ||||||||||||||||||||||||

| Junior subordinated debentures | 954 | 1,007 | 1,049 | 1,035 | 994 | ||||||||||||||||||||||||

| Other borrowings | 993 | 2,054 | 1,865 | 3,322 | 1,814 | ||||||||||||||||||||||||

| Total interest expense | 16,661 | 20,362 | 21,107 | 20,523 | 17,887 | ||||||||||||||||||||||||

| Net interest income | 86,094 | 89,694 | 87,833 | 88,678 | 84,383 | ||||||||||||||||||||||||

| Credit loss expense (benefit) | (607) | (1,764) | 4,284 | (702) | 1,330 | ||||||||||||||||||||||||

| Net interest income after credit loss expense (benefit) | 86,701 | 91,458 | 83,549 | 89,380 | 83,053 | ||||||||||||||||||||||||

| Noninterest income: | |||||||||||||||||||||||||||||

| Service charges on deposits | 1,212 | 1,483 | 1,847 | 1,742 | 1,596 | ||||||||||||||||||||||||

| Card income | 1,960 | 1,935 | 1,968 | 1,922 | 1,797 | ||||||||||||||||||||||||

| Net gains (losses) on sale of loans | 87 | 71 | 119 | 190 | 134 | ||||||||||||||||||||||||

| Net gains (losses) on disposal of premises and equipment | 606 | 14,265 | (3) | (218) | 846 | ||||||||||||||||||||||||

| Fee income | 13,735 | 13,478 | 14,305 | 12,755 | 9,114 | ||||||||||||||||||||||||

| Insurance commissions | 1,111 | (496) | 1,481 | 1,282 | 1,250 | ||||||||||||||||||||||||

| Other | 996 | (346) | 1,731 | 1,711 | 2,453 | ||||||||||||||||||||||||

| Total noninterest income | 19,707 | 30,390 | 21,448 | 19,384 | 17,190 | ||||||||||||||||||||||||

| Noninterest expense: | |||||||||||||||||||||||||||||

| Salaries and employee benefits | 58,168 | 55,086 | 60,192 | 59,882 | 58,718 | ||||||||||||||||||||||||

| Occupancy, furniture and equipment | 6,501 | 7,431 | 7,862 | 8,139 | 8,442 | ||||||||||||||||||||||||

| FDIC insurance and other regulatory assessments | 1,058 | 1,337 | 1,468 | 894 | 727 | ||||||||||||||||||||||||

| Professional fees | 4,763 | 4,286 | 5,228 | (320) | 6,064 | ||||||||||||||||||||||||

| Amortization of intangible assets | 2,516 | 2,826 | 2,956 | 3,400 | 2,400 | ||||||||||||||||||||||||

| Advertising and promotion | 1,212 | 1,689 | 2,209 | 1,838 | 1,464 | ||||||||||||||||||||||||

| Communications and technology | 13,119 | 12,911 | 12,295 | 12,315 | 12,244 | ||||||||||||||||||||||||

| Software amortization | 3,300 | 3,081 | 2,868 | 2,865 | 1,992 | ||||||||||||||||||||||||

| Travel and entertainment | 1,520 | 1,147 | 1,043 | 1,619 | 1,492 | ||||||||||||||||||||||||

| Other | 6,104 | 8,340 | 7,593 | 10,208 | 6,630 | ||||||||||||||||||||||||

| Total noninterest expense | 98,261 | 98,134 | 103,714 | 100,840 | 100,173 | ||||||||||||||||||||||||

| Net income before income tax | 8,147 | 23,714 | 1,283 | 7,924 | 70 | ||||||||||||||||||||||||

| Income tax expense | 1,792 | 4,500 | (425) | 3,504 | 53 | ||||||||||||||||||||||||

| Net income | $ | 6,355 | $ | 19,214 | $ | 1,708 | $ | 4,420 | $ | 17 | |||||||||||||||||||

| Dividends on preferred stock | (801) | (802) | (801) | (802) | (801) | ||||||||||||||||||||||||

| Net income available to common stockholders | $ | 5,554 | $ | 18,412 | $ | 907 | $ | 3,618 | $ | (784) | |||||||||||||||||||

15

Earnings per share:

| For the Three Months Ended | |||||||||||||||||||||||||||||

| (Dollars in thousands) | March 31, 2026 | December 31, 2025 | September 30, 2025 | June 30, 2025 | March 31, 2025 | ||||||||||||||||||||||||

| Basic | |||||||||||||||||||||||||||||

| Net income (loss) to common stockholders | $ | 5,554 | $ | 18,412 | $ | 907 | $ | 3,618 | $ | (784) | |||||||||||||||||||

| Weighted average common shares outstanding | 23,787,051 | 23,764,954 | 23,752,331 | 23,590,119 | 23,362,400 | ||||||||||||||||||||||||

| Basic earnings (loss) per common share | $ | 0.23 | $ | 0.77 | $ | 0.04 | $ | 0.15 | $ | (0.03) | |||||||||||||||||||

| Diluted | |||||||||||||||||||||||||||||

| Net income (loss) to common stockholders - diluted | $ | 5,554 | $ | 18,412 | $ | 907 | $ | 3,618 | $ | (784) | |||||||||||||||||||

| Weighted average common shares outstanding | 23,787,051 | 23,764,954 | 23,752,331 | 23,590,119 | 23,362,400 | ||||||||||||||||||||||||

| Dilutive effects of: | |||||||||||||||||||||||||||||

| Assumed exercises of stock options | 62,027 | 53,795 | 59,389 | 54,952 | — | ||||||||||||||||||||||||

| Restricted stock awards | — | — | — | 16,097 | — | ||||||||||||||||||||||||

| Restricted stock units | 125,664 | 102,264 | 90,675 | 89,156 | — | ||||||||||||||||||||||||

| Performance stock units - market based | 61,150 | 38,245 | 18,812 | 17,704 | — | ||||||||||||||||||||||||

| Employee stock purchase plan | 263 | 2,645 | 3,651 | 4,627 | — | ||||||||||||||||||||||||

| Weighted average shares outstanding - diluted | 24,036,155 | 23,961,903 | 23,924,858 | 23,772,655 | 23,362,400 | ||||||||||||||||||||||||

| Diluted earnings (loss) per common share | $ | 0.23 | $ | 0.77 | $ | 0.04 | $ | 0.15 | $ | (0.03) | |||||||||||||||||||

Shares that were not considered in computing diluted earnings per common share because they were antidilutive or have not met the thresholds to be considered in the dilutive calculation are as follows:

| For the Three Months Ended | |||||||||||||||||||||||||||||

| March 31, 2026 | December 31, 2025 | September 30, 2025 | June 30, 2025 | March 31, 2025 | |||||||||||||||||||||||||

| Stock options | 172,482 | 177,436 | 181,647 | 199,859 | 253,629 | ||||||||||||||||||||||||

| Restricted stock awards | — | — | — | — | 48,076 | ||||||||||||||||||||||||

| Restricted stock units | — | — | — | 5,171 | 203,812 | ||||||||||||||||||||||||

| Performance stock units - market based | — | 60,840 | 77,074 | 56,311 | 82,020 | ||||||||||||||||||||||||

| Employee stock purchase plan | — | — | — | — | — | ||||||||||||||||||||||||

Loans held for investment summarized as of:

| (Dollars in thousands) | March 31, 2026 | December 31, 2025 | September 30, 2025 | June 30, 2025 | March 31, 2025 | ||||||||||||||||||||||||

| Commercial real estate | $ | 724,923 | $ | 730,435 | $ | 769,314 | $ | 754,509 | $ | 811,244 | |||||||||||||||||||

| Construction, land development, land | 206,693 | 224,214 | 204,247 | 221,419 | 204,021 | ||||||||||||||||||||||||

| 1-4 family residential properties | 187,991 | 193,508 | 180,970 | 172,312 | 159,105 | ||||||||||||||||||||||||

| Farmland | 42,666 | 43,433 | 43,208 | 44,069 | 47,311 | ||||||||||||||||||||||||

| Commercial | 1,112,802 | 1,163,664 | 1,144,872 | 1,132,269 | 1,121,740 | ||||||||||||||||||||||||

| Factored receivables | 1,717,808 | 1,462,900 | 1,424,631 | 1,401,377 | 1,350,656 | ||||||||||||||||||||||||

| Consumer | 15,381 | 16,819 | 17,235 | 17,520 | 7,088 | ||||||||||||||||||||||||

| Mortgage warehouse | 1,180,875 | 1,156,334 | 1,202,445 | 1,209,695 | 965,058 | ||||||||||||||||||||||||

| Total loans | $ | 5,189,139 | $ | 4,991,307 | $ | 4,986,922 | $ | 4,953,170 | $ | 4,666,223 | |||||||||||||||||||

16

Our banking loan portfolio consists of traditional community bank loans as well as commercial finance product lines focused on businesses that require specialized financial solutions and national lending product lines that further diversify our lending operations.

Banking loans held for investment are further summarized below:

| (Dollars in thousands) | March 31, 2026 | December 31, 2025 | September 30, 2025 | June 30, 2025 | March 31, 2025 | ||||||||||||||||||||||||

| Commercial real estate | $ | 724,923 | $ | 730,435 | $ | 769,314 | $ | 754,509 | $ | 811,244 | |||||||||||||||||||

| Construction, land development, land | 206,693 | 224,214 | 204,247 | 221,419 | 204,021 | ||||||||||||||||||||||||

| 1-4 family residential | 187,991 | 193,508 | 180,970 | 172,312 | 159,105 | ||||||||||||||||||||||||

| Farmland | 42,666 | 43,433 | 43,208 | 44,069 | 47,311 | ||||||||||||||||||||||||

| Commercial - General | 303,561 | 313,696 | 285,571 | 298,653 | 274,697 | ||||||||||||||||||||||||

| Commercial - Agriculture | 44,396 | 42,588 | 49,742 | 48,107 | 49,529 | ||||||||||||||||||||||||

| Commercial - Equipment | 583,374 | 587,926 | 564,984 | 543,062 | 529,359 | ||||||||||||||||||||||||

| Commercial - Asset-based lending | 138,982 | 180,012 | 198,809 | 192,793 | 214,000 | ||||||||||||||||||||||||

| Commercial - Liquid Credit | 38,579 | 36,482 | 42,593 | 47,061 | 53,075 | ||||||||||||||||||||||||

| Consumer | 15,381 | 16,819 | 17,235 | 17,520 | 7,088 | ||||||||||||||||||||||||

| Mortgage Warehouse | 1,180,875 | 1,156,334 | 1,202,445 | 1,209,695 | 965,058 | ||||||||||||||||||||||||

| Total banking loans held for investment | $ | 3,467,421 | $ | 3,525,447 | $ | 3,559,118 | $ | 3,549,200 | $ | 3,314,487 | |||||||||||||||||||

The following table presents the Company’s operating segments:

| (Dollars in thousands) | Total | Corporate | ||||||||||||||||||||||||||||||||||||||||||

| Three Months Ended March 31, 2026 | Banking | Factoring | Payments | Intelligence | Segments | and Other(1) | Consolidated | |||||||||||||||||||||||||||||||||||||

| Total interest income | $ | 56,611 | $ | 38,944 | $ | 7,166 | $ | — | $ | 102,721 | $ | 34 | $ | 102,755 | ||||||||||||||||||||||||||||||

| Intersegment interest allocations | 5,731 | (8,219) | 2,488 | — | — | — | — | |||||||||||||||||||||||||||||||||||||

| Total interest expense | 15,039 | 6 | — | — | 15,045 | 1,616 | 16,661 | |||||||||||||||||||||||||||||||||||||

| Net interest income (expense) | 47,303 | 30,719 | 9,654 | — | 87,676 | (1,582) | 86,094 | |||||||||||||||||||||||||||||||||||||

| Credit loss expense (benefit) | (2,338) | 1,057 | 197 | — | (1,084) | 477 | (607) | |||||||||||||||||||||||||||||||||||||

| Net interest income after credit loss expense | 49,641 | 29,662 | 9,457 | — | 88,760 | (2,059) | 86,701 | |||||||||||||||||||||||||||||||||||||

| Noninterest income | 6,158 | 1,918 | 9,163 | 2,397 | 19,636 | 71 | 19,707 | |||||||||||||||||||||||||||||||||||||

| Noninterest expense: | ||||||||||||||||||||||||||||||||||||||||||||

| Salaries and employee benefits | 14,974 | 11,841 | 8,774 | 3,217 | 38,806 | 19,362 | 58,168 | |||||||||||||||||||||||||||||||||||||

| Depreciation | 1,577 | 288 | 176 | 16 | 2,057 | 826 | 2,883 | |||||||||||||||||||||||||||||||||||||

| Other occupancy, furniture and equipment | 2,016 | 496 | 141 | 27 | 2,680 | 938 | 3,618 | |||||||||||||||||||||||||||||||||||||

| FDIC insurance and other regulatory assessments | 1,058 | — | — | — | 1,058 | — | 1,058 | |||||||||||||||||||||||||||||||||||||

| Professional fees | 2,324 | 277 | 234 | 129 | 2,964 | 1,799 | 4,763 | |||||||||||||||||||||||||||||||||||||

| Amortization of intangible assets | 269 | 137 | 817 | 1,283 | 2,506 | 10 | 2,516 | |||||||||||||||||||||||||||||||||||||

| Advertising and promotion | 354 | 261 | 196 | 94 | 905 | 307 | 1,212 | |||||||||||||||||||||||||||||||||||||

| Communications and technology | 5,097 | 2,320 | 2,836 | 359 | 10,612 | 2,507 | 13,119 | |||||||||||||||||||||||||||||||||||||

| Software amortization | — | 1,070 | 1,821 | 58 | 2,949 | 351 | 3,300 | |||||||||||||||||||||||||||||||||||||

| Travel and entertainment | 229 | 230 | 293 | 146 | 898 | 622 | 1,520 | |||||||||||||||||||||||||||||||||||||

| Other | 3,444 | 670 | 816 | 71 | 5,001 | 1,103 | 6,104 | |||||||||||||||||||||||||||||||||||||

| Total noninterest expense | 31,342 | 17,590 | 16,104 | 5,400 | 70,436 | 27,825 | 98,261 | |||||||||||||||||||||||||||||||||||||

Net intersegment noninterest income (expense)(2) | 125 | 515 | (640) | — | — | — | — | |||||||||||||||||||||||||||||||||||||

| Operating income (loss) | $ | 24,582 | $ | 14,505 | $ | 1,876 | $ | (3,003) | $ | 37,960 | $ | (29,813) | $ | 8,147 | ||||||||||||||||||||||||||||||

17

| (Dollars in thousands) | Total | Corporate | ||||||||||||||||||||||||||||||||||||||||||

| Three Months Ended December 31, 2025 | Banking | Factoring | Payments | Intelligence | Segments | and Other(1) | Consolidated | |||||||||||||||||||||||||||||||||||||

| Total interest income | $ | 63,703 | $ | 39,336 | $ | 6,936 | $ | — | $ | 109,975 | $ | 81 | $ | 110,056 | ||||||||||||||||||||||||||||||

| Intersegment interest allocations | 5,903 | (8,682) | 2,779 | — | — | — | — | |||||||||||||||||||||||||||||||||||||

| Total interest expense | 18,686 | 7 | — | — | 18,693 | 1,669 | 20,362 | |||||||||||||||||||||||||||||||||||||

| Net interest income (expense) | 50,920 | 30,647 | 9,715 | — | 91,282 | (1,588) | 89,694 | |||||||||||||||||||||||||||||||||||||

| Credit loss expense (benefit) | (3,421) | 1,400 | 28 | — | (1,993) | 229 | (1,764) | |||||||||||||||||||||||||||||||||||||

| Net interest income after credit loss expense | 54,341 | 29,247 | 9,687 | — | 93,275 | (1,817) | 91,458 | |||||||||||||||||||||||||||||||||||||

| Noninterest income | 2,931 | 1,687 | 8,623 | 2,347 | 15,588 | 14,802 | 30,390 | |||||||||||||||||||||||||||||||||||||

| Noninterest expense: | ||||||||||||||||||||||||||||||||||||||||||||

| Salaries and employee benefits | 14,355 | 12,232 | 8,544 | 2,571 | 37,702 | 17,384 | 55,086 | |||||||||||||||||||||||||||||||||||||

| Depreciation | 1,583 | 348 | 182 | 14 | 2,127 | 1,146 | 3,273 | |||||||||||||||||||||||||||||||||||||

| Other occupancy, furniture and equipment | 1,997 | 468 | 141 | 16 | 2,622 | 1,536 | 4,158 | |||||||||||||||||||||||||||||||||||||

| FDIC insurance and other regulatory assessments | 1,337 | — | — | — | 1,337 | — | 1,337 | |||||||||||||||||||||||||||||||||||||

| Professional fees | 2,005 | 137 | 271 | (15) | 2,398 | 1,888 | 4,286 | |||||||||||||||||||||||||||||||||||||

| Amortization of intangible assets | 385 | 193 | 878 | 1,291 | 2,747 | 79 | 2,826 | |||||||||||||||||||||||||||||||||||||

| Advertising and promotion | 408 | 194 | 818 | 27 | 1,447 | 242 | 1,689 | |||||||||||||||||||||||||||||||||||||

| Communications and technology | 5,186 | 2,290 | 2,755 | 326 | 10,557 | 2,354 | 12,911 | |||||||||||||||||||||||||||||||||||||

| Software amortization | — | 1,014 | 1,684 | 30 | 2,728 | 353 | 3,081 | |||||||||||||||||||||||||||||||||||||

| Travel and entertainment | 133 | 119 | 227 | 202 | 681 | 466 | 1,147 | |||||||||||||||||||||||||||||||||||||

| Other | 4,450 | 765 | 1,758 | 210 | 7,183 | 1,157 | 8,340 | |||||||||||||||||||||||||||||||||||||

| Total noninterest expense | 31,839 | 17,760 | 17,258 | 4,672 | 71,529 | 26,605 | 98,134 | |||||||||||||||||||||||||||||||||||||

Intersegment noninterest income (expense)(2) | 138 | 502 | (640) | — | — | — | — | |||||||||||||||||||||||||||||||||||||

| Operating income (loss) | $ | 25,571 | $ | 13,676 | $ | 412 | $ | (2,325) | $ | 37,334 | $ | (13,620) | $ | 23,714 | ||||||||||||||||||||||||||||||

(1) Includes revenue and expense from the Company’s holding company, which does not meet the definition of an operating segment. Also includes corporate shared service costs such as the majority of salaries and benefits expense for our executive leadership team, as well as other selling, general, and administrative shared services costs including human resources, accounting, finance, risk management and a significant amount of information technology expense. For the three months ended December 31, 2025, noninterest income in the Corporate and Other category included a gain of $8.7 million on the sale of the building purchased in 2024 and a gain of $5.6 million on the sale of an aircraft.

(2) Intersegment noninterest income (expense) includes:

| (Dollars in thousands) | Banking | Factoring | Payments | |||||||||||||||||

| Three Months Ended March 31, 2026 | ||||||||||||||||||||

| Factoring revenue received from Payments | $ | — | $ | 911 | $ | (911) | ||||||||||||||

| Payments revenue received from Factoring | — | (287) | 287 | |||||||||||||||||

| Banking revenue received from Payments and Factoring | 125 | (109) | (16) | |||||||||||||||||

| Intersegment noninterest income (expense) | $ | 125 | $ | 515 | $ | (640) | ||||||||||||||

| Three Months Ended December 31, 2025 | ||||||||||||||||||||

| Factoring revenue received from Payments | $ | — | $ | 911 | $ | (911) | ||||||||||||||

| Payments revenue received from Factoring | — | (290) | 290 | |||||||||||||||||

| Banking revenue received from Payments and Factoring | 138 | (119) | (19) | |||||||||||||||||

| Intersegment noninterest income (expense) | $ | 138 | $ | 502 | $ | (640) | ||||||||||||||

18

Information pertaining to our Factoring segment, summarized as of and for the quarters ended:

| Factoring | March 31, 2026 | December 31, 2025 | September 30, 2025 | June 30, 2025 | March 31, 2025 | |||||||||||||||||||||||||||

| Factored receivable period end balance | $ | 1,404,958,000 | $ | 1,220,780,000 | $ | 1,193,849,000 | $ | 1,174,830,000 | $ | 1,146,429,000 | ||||||||||||||||||||||

| Commercial loans period end balance | $ | 3,910,000 | $ | 2,960,000 | $ | 3,173,000 | $ | 2,593,000 | $ | 1,080,000 | ||||||||||||||||||||||

Yield on average receivable balance(1) | 12.44 | % | 12.79 | % | 12.63 | % | 13.40 | % | 12.75 | % | ||||||||||||||||||||||

Current quarter charge-off rate(2) | 0.11 | % | 0.03 | % | 0.33 | % | (0.19 | %) | 0.11 | % | ||||||||||||||||||||||

| Factored receivables - transportation concentration | 96 | % | 97 | % | 96 | % | 96 | % | 97 | % | ||||||||||||||||||||||

| Interest income, including fees | $ | 38,944,000 | $ | 39,336,000 | $ | 37,157,000 | $ | 38,040,000 | $ | 33,331,000 | ||||||||||||||||||||||

| Noninterest income | 1,918,000 | 1,687,000 | 1,585,000 | 1,811,000 | 1,719,000 | |||||||||||||||||||||||||||

| Intersegment noninterest income | 911,000 | 911,000 | 911,000 | 910,000 | 911,000 | |||||||||||||||||||||||||||

| Factoring total revenue | 41,773,000 | 41,934,000 | 39,653,000 | 40,761,000 | 35,961,000 | |||||||||||||||||||||||||||

| Average net funds employed | 1,197,257,000 | 1,143,597,000 | 1,097,229,000 | 1,065,073,000 | 948,729,000 | |||||||||||||||||||||||||||

Yield on average net funds employed(1) | 14.15 | % | 14.55 | % | 14.34 | % | 15.35 | % | 15.37 | % | ||||||||||||||||||||||

| Operating income (loss) | $ | 14,505,000 | $ | 13,676,000 | $ | 8,212,000 | $ | 19,754,000 | $ | 6,919,000 | ||||||||||||||||||||||

| Factoring total revenue | $ | 41,773,000 | $ | 41,934,000 | $ | 39,653,000 | $ | 40,761,000 | $ | 35,961,000 | ||||||||||||||||||||||

Operating margin(1) | 34.72 | % | 32.61 | % | 20.71 | % | 48.46 | % | 19.24 | % | ||||||||||||||||||||||

| Accounts receivable purchased | $ | 3,262,610,000 | $ | 3,119,443,000 | $ | 2,997,895,000 | $ | 2,873,659,000 | $ | 2,707,805,000 | ||||||||||||||||||||||

| Number of invoices purchased | 1,683,160 | 1,744,811 | 1,735,860 | 1,697,851 | 1,497,644 | |||||||||||||||||||||||||||

| Average invoice size | $ | 1,938 | $ | 1,788 | $ | 1,727 | $ | 1,693 | $ | 1,808 | ||||||||||||||||||||||

| Average invoice size - transportation | $ | 1,897 | $ | 1,751 | $ | 1,690 | $ | 1,663 | $ | 1,769 | ||||||||||||||||||||||

| Average invoice size - non-transportation | $ | 5,609 | $ | 4,470 | $ | 4,381 | $ | 3,638 | $ | 4,019 | ||||||||||||||||||||||

(1)Operating margin is a non-GAAP financial measure used as a supplemental measure to evaluate the performance of our Factoring segment. For the three months ended June 30, 2025, operating income and factoring total revenue were impacted by $1.2 million of interest and fees resulting from the USPS Settlement and such settlement further impacted operating income by $7.4 million of legal expense accrual reversal and $3.8 million of recovery of factoring balances charged-off in a prior period. Operating income for the three months ended June 30, 2025 was also impacted by a $2.0 million legal settlement that was unrelated to the USPS Settlement. Such items had a 24.71% impact on operating margin, a 0.43% impact on yield on average receivables, and a 0.46% impact on yield on average net funds employed for the three months ended June 30, 2025.

(2)The current quarter charge-off rate for the three months ended June 30, 2025 reflects a $3.8 million recovery of factoring balances charged off in a prior period. Such recovery impacted the current quarter charge-off rate for that period by (0.33%).

19

Information pertaining to our Payments segment, summarized as of and for the quarters ended:

| Payments | March 31, 2026 | December 31, 2025 | September 30, 2025 | June 30, 2025 | March 31, 2025 | |||||||||||||||||||||||||||

| Supply chain financing factored receivables | $ | 222,168,000 | $ | 174,292,000 | $ | 157,662,000 | $ | 152,054,000 | $ | 122,583,000 | ||||||||||||||||||||||

| Quickpay and other factored receivables | 90,682,000 | 67,828,000 | 73,120,000 | 74,493,000 | 81,644,000 | |||||||||||||||||||||||||||

| Total factored receivable period end balance | $ | 312,850,000 | $ | 242,120,000 | $ | 230,782,000 | $ | 226,547,000 | $ | 204,227,000 | ||||||||||||||||||||||

| Total revenue | ||||||||||||||||||||||||||||||||

| Supply chain finance interest income | $ | 4,192,000 | $ | 4,177,000 | $ | 3,895,000 | $ | 3,412,000 | $ | 2,695,000 | ||||||||||||||||||||||

| Quickpay interest income | 2,974,000 | 2,759,000 | 2,874,000 | 2,818,000 | 2,668,000 | |||||||||||||||||||||||||||

| Intersegment interest income allocation | 2,488,000 | 2,779,000 | 2,943,000 | 2,896,000 | 2,918,000 | |||||||||||||||||||||||||||

| Total interest income | 9,654,000 | 9,715,000 | 9,712,000 | 9,126,000 | 8,281,000 | |||||||||||||||||||||||||||

| Broker noninterest income | 7,820,000 | 7,330,000 | 7,131,000 | 6,443,000 | 5,178,000 | |||||||||||||||||||||||||||

| Factor noninterest income | 796,000 | 952,000 | 933,000 | 993,000 | 1,233,000 | |||||||||||||||||||||||||||

| Other noninterest income | 547,000 | 341,000 | 398,000 | 288,000 | 120,000 | |||||||||||||||||||||||||||

| Intersegment noninterest income | 287,000 | 290,000 | 329,000 | 381,000 | 372,000 | |||||||||||||||||||||||||||

| Total noninterest income | 9,450,000 | 8,913,000 | 8,791,000 | 8,105,000 | 6,903,000 | |||||||||||||||||||||||||||

| $ | 19,104,000 | $ | 18,628,000 | $ | 18,503,000 | $ | 17,231,000 | $ | 15,184,000 | |||||||||||||||||||||||

| Total expense | ||||||||||||||||||||||||||||||||

| Credit loss expense (benefit) | $ | 197,000 | $ | 28,000 | $ | 9,000 | $ | 92,000 | $ | 118,000 | ||||||||||||||||||||||

| Noninterest expense | 16,104,000 | 17,258,000 | 17,094,000 | 16,844,000 | 17,113,000 | |||||||||||||||||||||||||||

| Intersegment noninterest expense | 927,000 | 930,000 | 950,000 | 949,000 | 944,000 | |||||||||||||||||||||||||||

| $ | 17,228,000 | $ | 18,216,000 | $ | 18,053,000 | $ | 17,885,000 | $ | 18,175,000 | |||||||||||||||||||||||

| Pre-tax operating income (loss) | $ | 1,876,000 | $ | 412,000 | $ | 450,000 | $ | (654,000) | $ | (2,991,000) | ||||||||||||||||||||||

| Depreciation expense | 176,000 | 182,000 | 203,000 | 222,000 | 230,000 | |||||||||||||||||||||||||||

| Software amortization expense | 1,821,000 | 1,684,000 | 1,550,000 | 1,413,000 | 1,196,000 | |||||||||||||||||||||||||||

| Intangible amortization expense | 817,000 | 878,000 | 904,000 | 1,418,000 | 1,551,000 | |||||||||||||||||||||||||||

Earnings (losses) before interest, taxes, depreciation, and amortization(1) | $ | 4,690,000 | $ | 3,156,000 | $ | 3,107,000 | $ | 2,399,000 | $ | (14,000) | ||||||||||||||||||||||

EBITDA Margin(1) | 24.5 | % | 16.9 | % | 16.8 | % | 13.9 | % | (0.1) | % | ||||||||||||||||||||||

| Number of invoices processed | 8,220,371 | 9,053,274 | 8,826,848 | 8,500,565 | 7,182,044 | |||||||||||||||||||||||||||

| Amount of payments processed | $ | 11,014,040,000 | $ | 10,995,478,000 | $ | 10,662,418,000 | $ | 10,081,206,000 | $ | 8,777,825,000 | ||||||||||||||||||||||

| Network invoice volume | 1,043,488 | 1,090,848 | 1,057,606 | 1,004,603 | 719,531 | |||||||||||||||||||||||||||

| Network payment volume | $ | 1,941,127,000 | $ | 1,829,509,000 | $ | 1,696,817,000 | $ | 1,579,662,000 | $ | 1,167,464,000 | ||||||||||||||||||||||

| LoadPay | ||||||||||||||||||||||||||||||||

| Revenue | $ | 437,000 | $ | 345,000 | $ | 218,000 | $ | 92,000 | $ | 24,000 | ||||||||||||||||||||||

| Pre-tax operating income (loss) | $ | (2,059,000) | $ | (2,584,000) | $ | (2,353,000) | $ | (1,751,000) | $ | (1,053,000) | ||||||||||||||||||||||

| Depreciation expense | 21,000 | 21,000 | 20,000 | 16,000 | 3,000 | |||||||||||||||||||||||||||

| Software amortization expense | 374,000 | 324,000 | 289,000 | 251,000 | 140,000 | |||||||||||||||||||||||||||

Earnings (losses) before interest, taxes, depreciation, and amortization(1) | $ | (1,664,000) | $ | (2,239,000) | $ | (2,044,000) | $ | (1,484,000) | $ | (910,000) | ||||||||||||||||||||||

| Payments revenue excluding LoadPay | $ | 18,667,000 | $ | 18,283,000 | $ | 18,285,000 | $ | 17,139,000 | $ | 15,160,000 | ||||||||||||||||||||||

Payments EBITDA excluding LoadPay(2) | $ | 6,354,000 | $ | 5,395,000 | $ | 5,151,000 | $ | 3,883,000 | $ | 896,000 | ||||||||||||||||||||||

Payments EBITDA Margin excluding LoadPay(2) | 34.0 | % | 29.5 | % | 28.2 | % | 22.7 | % | 5.9 | % | ||||||||||||||||||||||

20

(1)Earnings (losses) before interest, taxes, depreciation, and amortization ("EBITDA") and EBITDA margin are non-GAAP financial measures used as supplemental measures to evaluate the performance of our Payments segment. EBITDA is useful because it provides a clearer view of underlying operating performance by excluding the effects of capital structure, tax regimes, and non-cash depreciation and amortization. EBITDA margin complements EBITDA by illustrating how efficiently revenue is converted into operating profitability.

(2)Payments EBITDA excluding LoadPay and Payments EBITDA Margin excluding LoadPay are non-GAAP financial metrics used as supplemental measures to evaluate the performance of our Payments segment exclusive of the investments associated with LoadPay, which is a relatively new product in its early stages. Such adjusted EBITDA measures provide comparable clarity into the performance of our Payments segment prior to the advent of our LoadPay product.

Information pertaining to our Intelligence segment, summarized as of and for the quarters ended:

| Intelligence | March 31, 2026 | December 31, 2025 | September 30, 2025 | |||||||||||||||||

| Revenue | $ | 2,397,000 | $ | 2,347,000 | $ | 2,338,000 | ||||||||||||||

| Cost of revenue | 333,000 | 283,000 | 266,000 | |||||||||||||||||

| Gross profit | 2,064,000 | 2,064,000 | 2,072,000 | |||||||||||||||||

| Selling, general and administrative costs | 5,067,000 | 4,389,000 | 5,670,000 | |||||||||||||||||

| Pre-tax operating income (loss) | $ | (3,003,000) | $ | (2,325,000) | (3,598,000) | |||||||||||||||

Gross Margin(1) | 86 | % | 88 | % | 89 | % | ||||||||||||||

*prior periods not meaningful